Retail investing hit its zeitgeist moment in 2020 and interest continues to soar. As I write this in January 2021, google search trends show “investing” is at its second highest peak in the last 16 years, with the highest peak being March 2020. Similar trends can be seen for “call options” and “day trading.”

The actuals back this sentiment up. Individual stock trading is at a 10-year high, with “retail trades at 19.5% of all US order flow (June 2020)” (compared to 10%, 2010 and 15%, 2019). Retail investing also surged before the 2000s dotcom bust and 2008 recession — but unlike the 2000 bubble, companies have real revenues. This isn’t just a trend of the wealthy either: people earning $35–50k per year traded 93% more stocks the week after receiving a stimulus check.

2020 also saw Robinhood become a household name by minimizing friction points including fees and minimums. With Robinhood’s rise to prominence has come the consumerization of equities trading, formerly a field dominated by institutional investors and high net worth individuals that relegated the average consumer to robo-advisors or (formerly) costly Schwab/ Fidelity/ TDAmeritrade accounts (most have introduced free services since 2017).

So where do we go from here? Some say the window for retail investing products is over. I disagree. Robinhood’s dominance marks the beginning of a new generation of retail investment products. As of 2020, millennials owned just 3% of all retail equity and 43% to 51% didn’t own stock in 2019. The last few decades saw 4–5 dominant brokerages so there is still room for new players to acquire investors and increase wallet share. Millennials hit 10T in assets but are still underinvested in equities relative to older generations.

In the next decade we will see a new generation of investing brands fight to become the primary brokerage for Millennials and GenZ. Why? Robinhood’s success awakened the investment mindset amongst Millennials/GenZ, and it’s not just equities. It’s trading cards, fine wine, vacation homes, streetwear, and other lifestyle assets turned investments.

Newer entrants will integrate into fintech and commerce companies as investing moves from being part of the goods & services economy to part of the experience & transformational economies.

This post outlines a few key trends enabling the consumerization of retail investing, what this means for key players in the industry, and what the next generation of startups serving consumers will have to get right.

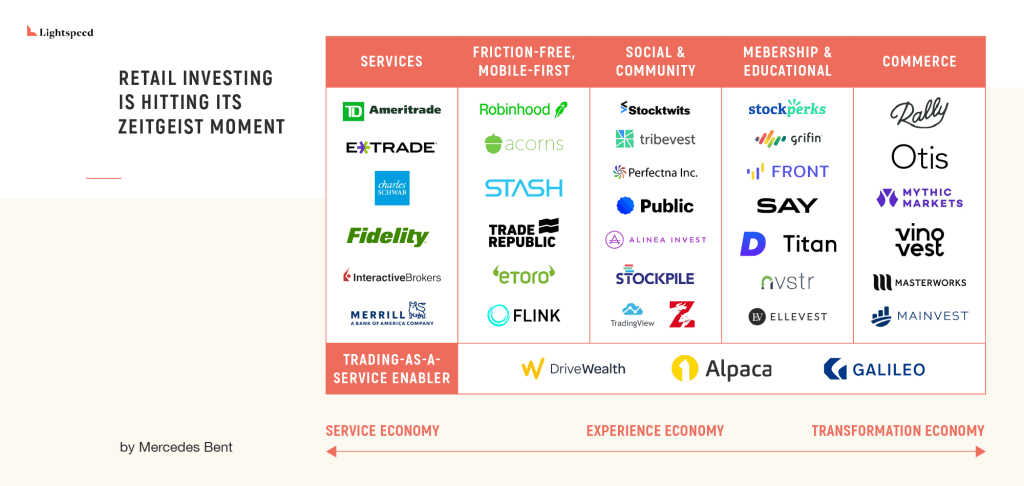

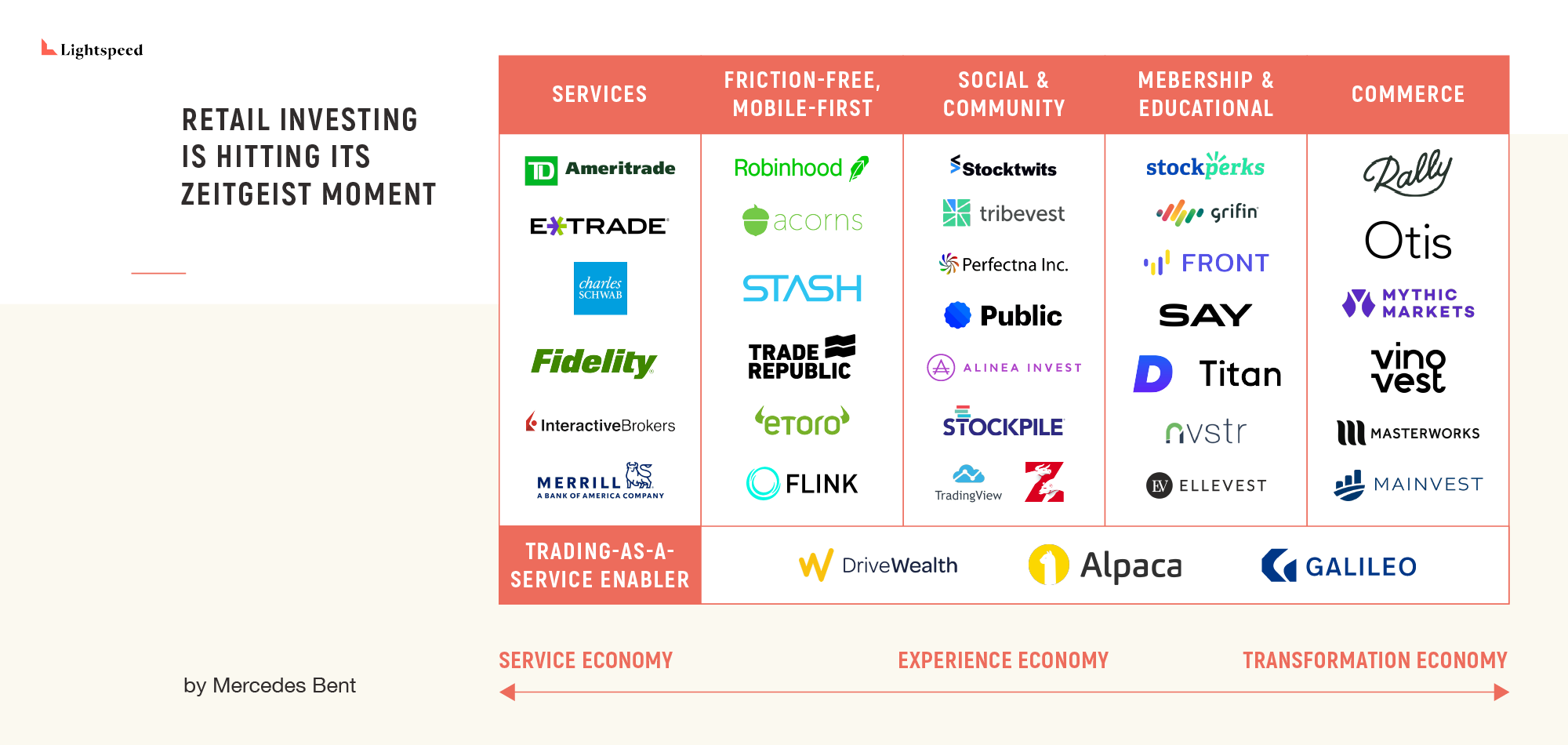

The consumerization of retail investing has been enabled by the following trends:

- Removal of friction points & a move to competing on user experience — Robinhood made no commission/fees, no minimums, and fractional investing table stakes for new brokerage entrants. No longer competing on access to basic services, investing brokerages must now deliver enhanced user experiences that leave customers feeling empowered with greater wealth and more knowledge.

- Gamification of trading — Trading is in many ways, like a sport, and Robinhood made it even more so by incentivizing activity and giving away free stock to users who scratched a lottery-like ticket. Robinhood and 2020’s gravity-defying stock market made watching the stocks a national pass-time (“dude, did you see where Tesla’s at today??”) and eyeballs waiting to be entertained flocked to trading platforms.

- Open APIs dedicated to brokerage and investment — Drivewealth, Alpaca, Galileo and more are enabling fintechs to more easily launch trading services with their open brokerage APIs. By making it easier for anyone to start a trading platform, entrepreneurs can focus more on front-end features that enhance the trading experience and less on the nuts and bolts.

- Increased leisure time and fewer activities with Covid — The search term “investing” exploded at the beginning of the pandemic because consumers had nowhere to go and were able to take some control back over their lives by using trading as a predictive outlet of the world unraveling around them.

What this means for key players in the industry:

- Neobanks and horizontal fintechs will add investing products — Investing functionality is becoming a core feature of many consumer and commerce experiences, fintech or not. Every new fintech will need to consider adding investing as a product to their suite of debit and credit products.

- Brokerages must innovate and compete on the user experience — The next generation will compete by driving deeper social/community experiences. As we’ve seen in several industries (RE,AM), newer entrants grab market share by lowering or eliminating fees, which commoditizes access and forces incumbents to compete on new dimensions that startups excel at, such as a more robust user experience.

- Investor Relations teams will become customer experience teams — Growing interest and means IR teams will need to deepen relationships with retail investors. Historically IR teams’ focus has been institutional investors. These teams will need to become customer experience and advocate teams and align with marketing/UX teams.

- Every commerce company can offer investment services — In the same way any company can become a fintech by extending banking services — (payment integration), any commerce brand can become an investment platform thanks to open investing APIs such as Galileo or Drivewealth. In the future, brands will offer fractional investing in special edition collectibles. The first wave has seen everything from wine to shoes to art to baseball cards with RallyRoad, Otis, Vinovest and more.

- Fintech media seeing new entrants — I watched CNBC’s Squawk Box every morning a decade ago when I worked at Goldman. Today Barstool’s Dave Portnoy has become a fan favorite investing $5M of his own money and famously says “stocks only go up right”. New fintech media entrants such as Dave and Lauren Simmons will be the new face of retail investing.

What will the next generation of startups serving consumers have to get right? Here’s what consumers are craving and how startups are stepping up to serve them:

- Insights and Education — Investors want to feel informed about their trading choices, and with 80% of day traders losing money, and only 37% of millennials feel knowledgeable about investing, they need it. It’s also a signal. Talking about insights from your broker’s newsletter is the new Economist magazine on your coffee table. Educational-investing doubles as conspicuous consumption and Nvstr, Front and active manager TitanVest know this.

- Membership — Consumers are technically owners of stocks — but when’s the last time you felt like you had the right to a discount or perk because you owned some? Even when the do offer perks, there’s no easy portal. In the future retail investors will expect to have a relationship with the company behind the stock. Several startups are deepening that relationship including Grifin and Stockperks.

- Social connectedness & community. Why doesn’t trading feel more like a social network? CNBC and Shark Tank show us there’s a mainstream (TV) appetite for investment-related media. Stock holders already generate and consume content, discuss it with others, compare themselves, post their wins, and follow influencers who excel at their craft. Companies to watch: Zingeroo, Public.com, Alinea, Perfectna, TradingView

- Women-friendly platforms — Major trading platforms are 70% male. As my partner Jeremy is oft to say, women are often early adopters of consumer platforms that become part of pop culture. I expect we’ll see droves of women join investment platforms in the coming years. Ellevest has led the way here and more are coming with Alinea and others.

- Gamification 2.0 — Investing is like a sport — it involves practice, competitiveness, and winning. Traders get a rush of adrenaline, real time results, and have the ability to work as a team or solo. For most retail investors, trading has not truly been a team sport. The next generation of companies will specialize in game design and game mechanics and create team experiences to rival any sport. Companies doing this already include Zingeroo, Robinhood and more.

- Commerce — Consumers want to feel more connected to their investments. Retail investors overindex in mega brand names (22%) (compared to 10% overall levels in 2019) because they feel they know the brand. Sites such as RallyRoad, Mythic Markets, & Masterworks combine the best of e-commerce and investing. The consumerization of investing leads to better UX, and the investmentization of commerce will lead to stickier, repeat brand ambassadors.

Some have pointed out that we’re still in a tremendously long bull market and that the music will stop for retail investing when we enter a true bear and when investors lose money. After all, we saw households pull back over 30% in equities as a share of their assets during the 2008 recession and extensive research shows it’s hard to beat the market (85% of large-cap actively managed funds underperformed the S&P over the last 10 years).

They’re right — overall retail trading volumes will decline and share of wallet will momentarily decline. However a new generation of investors that chose platforms will remain sticky (overall equity participation is relatively steady, +/ 7% last few decades).

Investors still need to choose where to invest, millennials are still underinvested, and experience-based platforms will win. My thesis is about the next decade of retail investors, not a specific 1–2 year recessionary period.

Long-term, the investing mindset persists against short-term losses* because investing is about more than bets or entertainment. Investing is about giving people the feeling that they can achieve the American dream, that they too can achieve economic and social mobility. There are four things we can do with a dollar: spend it, save it, invest it, or donate it — and investing evokes some of the strongest emotions.

If you’re a founder building a next-generation investment platform and you’re crazy about consumers, please get in touch, I’d love to know what you’re building: mbent@lsvp.com

* The behavioral economist side of me feels compelled to point out that risk-aversion is real and short-term investment choices are affected by losses

Leave a comment