Foreword: I’ve long been a mentor of startups in the Entrepreneurship and VC class at Stanford. Recently I was hosting several GSB students from the class who were working on a lending startup, and we got to “whiteboarding.” Well, napkin writing. I shared my lending mental model with them and realized I’ve never encapsulated it before. Here it goes:

For lenders, net interest margin (NIM) is the name of the game. The wider your spread, the bigger your edge. It’s the end-all-be-all metric, next to NPLs.

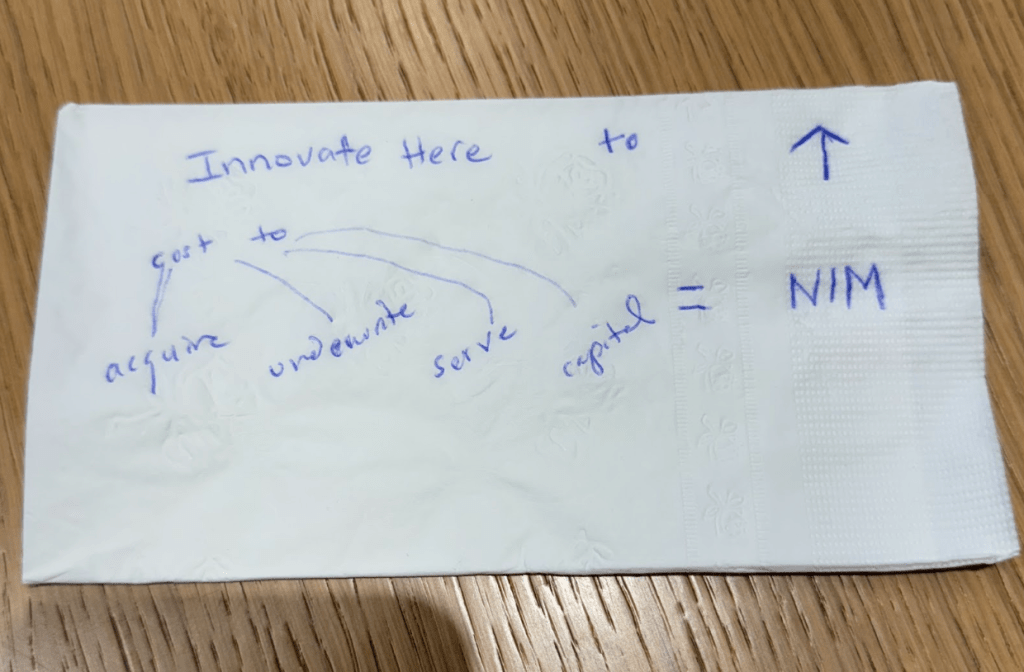

I’m on the board of a lending unicorn and have met hundreds of lending companies. My lending mental model is that NIM can be strategically widened by innovating in specific input areas.

There are four key components of a lending business that, when improved, can trigger huge NIM advantages across the balance sheet.

1. Cost to acquire – How efficiently can you bring in new customers?

2. Cost to underwrite – How effectively can you assess customer risk?

3. Cost to serve – How cheaply can you operate your products and retain your customers?

4. Cost of capital – How low can you drive funding costs?

Customer Acquisition: The growth advantage

For decades, banks relied on physical branch networks to acquire customers. Then fintech came along, proving you could scale without expensive real estate. But CAC is still a significant line item in lending unit economics. Every lender today needs an unfair advantage in how they acquire customers.

A great example is Robinhood (I know what you’re thinking – they’re not a lender!). Robinhood is a lending example because cross-selling users is a form of an internal CAC advantage for X1. By acquiring the credit card X1, Robinhood positioned themselves to cross-sell lending products to their existing user base. Their next move could even be a stock-secured lending model, allowing customers to borrow against their portfolio—further reducing risk and capital costs. This efficiency is compounded and more costs offset by a subscription model where only “Gold” members can apply for X1 — that’s $5 a month.

(FWIW: Robinhood’s investing side also had a CAC advantage – their core innovation was branded “commission-free trading” but was really a monetization innovation, shifting costs to market makers through payment for order flow (PFOF)).

A second example is Aven, a fintech that’s redefining home equity lending. It made underwriting almost frictionless by inventing a digitlal process to confirm remote wet signatures. Before HELOC sellers needed homeowners to sign in person. Aven brought “ink” online so that regulators could approve their systems without changing legislation – a technological leap that made formerly resource-constrained lending operations scalable. This massively reduces the CAC if you can acquire customers online versus needing an in-person signature.

Cost to Underwrite / Cost of Risk: The data advantage

Affirm is a great example of innovation in lowering the cost of risk.

Traditional credit card companies assess their risk at the moment of an account opening, but Affirm underwrites at the point of transaction. Instead of taking a broad risk view across all customer spending, they are able to instead:

1. Sit with the merchant, not the consumer—giving them deep transaction-level data.

2. Underwrite each individual purchase, making their model more, and more precise.

3. Boost efficiency by underwriting resources only when a transaction is actually happening.

This is the opposite of unsecured credit card models, which use past behavior to predict future behavior. But Affirm’s model allows them to understand PRESENT behavior.

Another example is Stori, a Mexican credit card startup I invested in and am on the board of. They’ve extended credit to millions of people in Mexico who never had credit before using non-traditional signals like mobile phone usage, online spending activity, and many more proprietary variables.

Cost to Serve: The love advantage

Cost to serve includes customer support, collections, and anything to service a lending customer. Most lenders see customer support as a money pit. Good ones see it as a moat. Great ones see it as revenue-generating customer love.

Why? Because customer satisfaction directly reduces servicing costs in three ways:

1. Fewer charge-offs and delinquencies – Happy customers are more likely to repay.

2. Lower churn – Retained customers are cheaper than acquiring new ones.

3. More organic referrals – Strong NPS means lower CAC.

Nubank famously has an extreme focus on customer experience, which has actually resulted in an NPS score for Nubank that is higher than Apple’s – Nubank’s NPS is 90 compared to an NPS of 72.

Nubank prioritizes customers while Apple prioritizes products. As a lender, Nubank invests in this because it knows that its reputation and its revenue are forever linked.

Nubank customers self-serve more efficiently, reducing costly service calls. They use gamification mechanics (like milestones and rewards) to make customers feel invested in their financial progress. And their brand marketing is transparent and consumer-focused without crossing the cringe line.

Cost of Capital: The cash advantage

At the end of the day, lending is a spread business. It’s matchmaking capital markets. And what’s the biggest innovation in capital markets right now? Tokenization.

Figure is leading the charge here by:

– Tokenizing mortgages on blockchain, allowing them to be traded in new ways.

– Using the Providence Blockchain to create faster, more transparent securitization.

– Growing the pool of capital providers well beyond traditional institutions.

This is the same Mike Cagney (founder of SoFi) who saw an opportunity to use securitization to drive down borrowing costs for student loans. Now, he’s applying the same strategy to home equity. And it paid of:

- By the end of 2022, Figure had originated over $5 billion in HELOCs, assisting more than 70,000 households across the United States.

- In April 2023, Figure completed its first publicly rated HELOC asset-backed securitization, underwritten by major financial institutions including Jefferies, Goldman Sachs, and J.P. Morgan. This transaction involved 3,568 loans with a total unpaid principal balance of $236.8 million.

- Today, Figure’s integration of technology has significantly reduced the time required for HELOC processing, enabling loan decisions in as few as five minutes and funding in as little as five days.

Even JPMorgan is moving into tokenized lending, proving this isn’t just a startup experiment—it’s the almost-certain future of markets.

Lending isn’t about incremental improvements—it’s about structural advantages derived from key levers.

Innovating in one of these 4 areas by leveraging a technological breakthrough is also what creates differentiation from traditional lenders.

Leave a reply to Akhil Kishore Cancel reply